KEEP ELIGIBLE MEMBERS COVERED

A buyer's guide to Medicaid coverage continuity, administrative churn, and the emerging infrastructure built to prevent it.

SOCIAL CARE CATEGORY: COVERAGE CONTINUITY

CATEGORY STAGE: DEVELOPING ⇈

WHY THIS MATTERS NOW

Coverage continuity is becoming one of the most financially consequential operational challenges in Medicaid.

The Medicaid unwinding demonstrated that many members lost coverage for procedural reasons. Millions of disenrollments occurred for procedural reasons, exposing plans, providers, and states to enrollment disruption, reimbursement loss, and increased administrative burden.

The next phase of Medicaid policy is likely to increase those pressures.

Current drivers include:

Six-month renewals beginning for expansion populations in 2027

Increased administrative workload for plans and state agencies

Unlike many social-care categories, coverage continuity does not depend on long-term utilization reduction to demonstrate value.

For providers, the pathway is equally direct:

Coverage Restored → Reduced Self-Pay Exposure → Recovered Reimbursement

This makes coverage continuity one of the few social-care categories where financial impact can often be evaluated within the same contract cycle.

WHAT MAKES THIS A CATEGORY?

While the organizations in this category operate at different points in the eligibility lifecycle, they are responding to the same operational and financial problem: coverage loss among individuals who remain eligible for Medicaid.

BeneLynk focuses on benefits continuity, helping members maintain enrollment in programs such as Medicaid, MSP, LIS, and other eligibility-dependent benefits. Centauri concentrates on eligibility optimization and recovery, supporting dual-eligible enrollment, disability qualification, and benefit preservation. Fortuna is oriented toward renewal completion, document collection, notice management, and member navigation through increasingly complex renewal processes. Agilian focuses on identifying members at risk of procedural disenrollment and intervening before coverage is lost.

The workflows differ, but each organization is attempting to influence the same set of outcomes: completed renewals, successful verification, restored eligibility, reduced procedural disenrollment, and continuity of coverage.

From a buyer perspective, these activities affect a common set of economic variables. For managed care organizations, coverage continuity preserves member months, premium revenue, capitation payments, risk-adjustment opportunities, and care-management attribution. For providers, it reduces uncompensated care exposure and improves reimbursement capture. For state agencies, it reduces administrative burden associated with disenrollment, reenrollment, appeals, and eligibility processing.

Historically, these functions were often addressed through separate operational teams, vendor relationships, or manual workflows. As renewal frequency increases, verification requirements expand, and administrative complexity grows, organizations are beginning to evaluate them as components of a broader coverage-continuity strategy. The result is the emergence of a procurement category centered on maintaining eligibility, preserving enrollment, and reducing administrative churn across the Medicaid population.

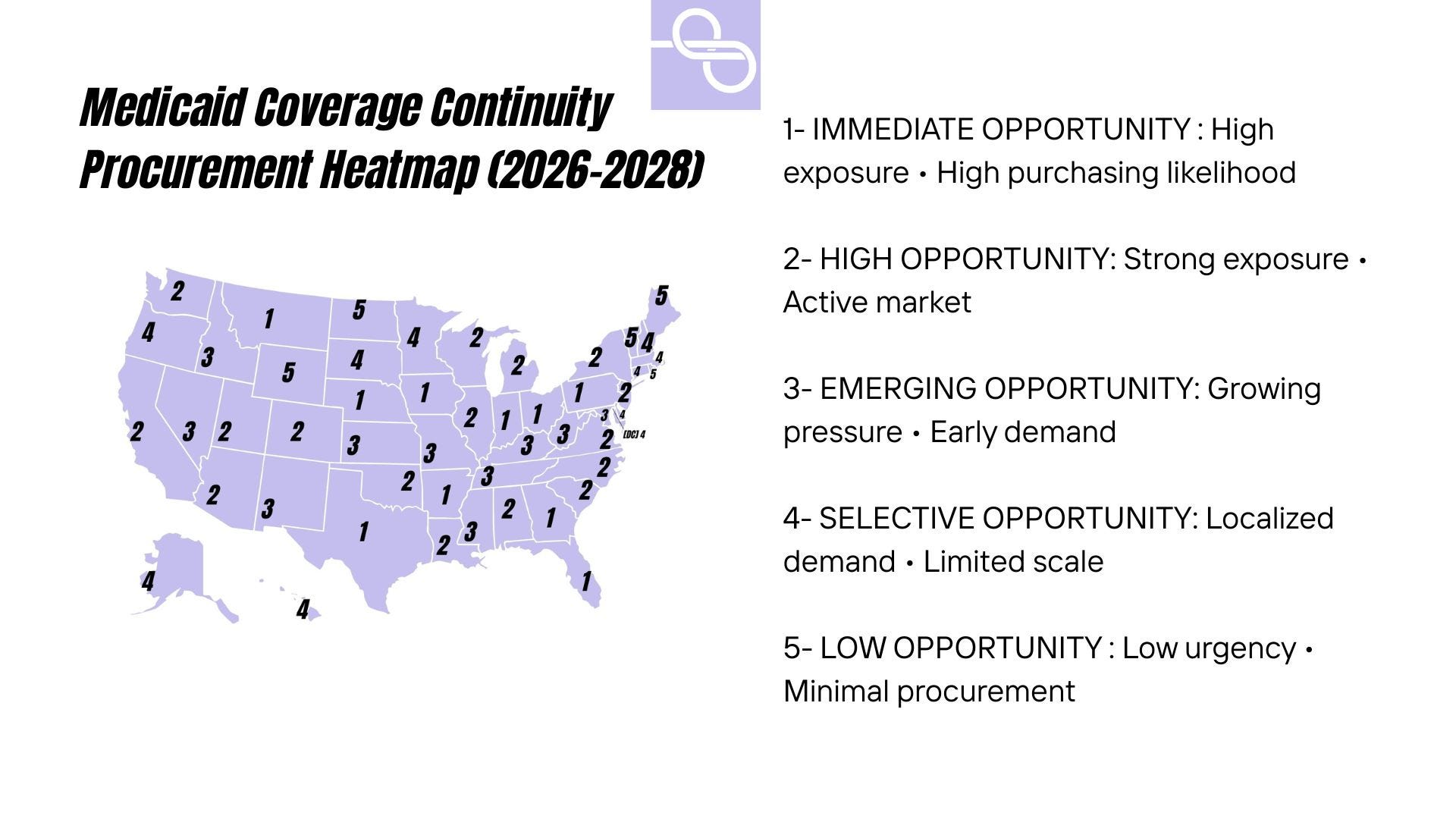

MEDICAID COVERAGE CONTINUITY OPPORTUNITY MAP

Administrative churn, renewal complexity, work requirements, verification activity, and managed care exposure vary significantly by state. As a result, procurement demand for coverage continuity infrastructure is likely to concentrate in specific markets over the next 24 months.

The map below identifies states where coverage continuity is most likely to become a purchasing decision rather than simply an operational challenge.

Tier Definitions

🟣 Tier 1 — Immediate Opportunity

High exposure • High purchasing likelihood

🟣 Tier 2 — High Opportunity

Strong exposure • Active market

🟣 Tier 3 — Emerging Opportunity

Growing pressure • Early demand

🟣 Tier 4 — Selective Opportunity

Localized demand • Limited scale

⚪ Tier 5 — Low Opportunity

Low urgency • Minimal procurement

Tier 1: Immediate Opportunity

These states combine significant Medicaid enrollment, administrative churn pressure, policy-driven eligibility complexity, and active procurement environments.

Arkansas

Florida

Georgia

Indiana

Iowa

Montana

Nebraska

Ohio

Pennsylvania

Texas

Tier 2: High Opportunity

Large populations, meaningful administrative exposure, and growing procurement readiness.

Alabama

Arizona

California

Colorado

Illinois

Louisiana

Michigan

New Jersey

New York

North Carolina

Oklahoma

South Carolina

Utah

Virginia

Washington

Wisconsin

Tier 3: Emerging Opportunity

Operational pressure is building, but procurement activity remains less mature.

Idaho

Kansas

Kentucky

Maryland

Mississippi

Missouri

Nevada

New Mexico

Tennessee

West Virginia

Tier 4: Selective Opportunity

Coverage continuity remains relevant but purchasing activity is likely to be targeted and localized.

Alaska

Connecticut

Delaware

District of Columbia

Hawaii

Massachusetts

Minnesota

New Hampshire

Oregon

South Dakota

Tier 5: Low Opportunity

Smaller populations, lower churn exposure, or limited near-term procurement pressure.

Maine

North Dakota

Rhode Island

Vermont

Wyoming

What This Means

Not all Medicaid churn creates the same purchasing environment.

Some states face significant coverage instability but have limited procurement pathways. Others combine administrative pressure, financial exposure, managed care incentives, and active contracting environments that make coverage continuity investments increasingly attractive.

The strongest near-term opportunities appear concentrated in states where policy pressure, enrollment scale, and reimbursement exposure are converging simultaneously.

These states are likely to define the next generation of coverage continuity procurement.

TOP SOLUTIONS

Pull Score: 24 / 31

Trend: ⇈

Position: Category Incumbent

Strengths

Strongest visible procurement footprint in the category

National payer relationships

24M+ members supported

Benefits continuity expertise

Immediate reimbursement preservation logic

Watch

Limited independent outcome validation

Pricing opacity

Pull Score: 24 / 31

Trend: ⇈

Position: Enterprise Infrastructure

Strengths

60+ health plans

60M+ covered lives

Dual eligibility optimization

LIS/MSP/SSI enrollment expertise

Large-scale reimbursement preservation

Watch

Methodology transparency

Limited payer-authored validation

Pull Score: 26 / 31

Trend: ⇈

Position: Administrative Churn Infrastructure

Strengths

Reinstatement and churn-recovery focus

Reported capitation preservation outcomes

Same-cycle revenue protection logic

MMIS-integrated workflows

Watch

Limited public contract visibility

Independent validation remains limited

Pull Score: 25 / 31

Trend: ⇈

Position: Renewal & Eligibility Continuity Platform

Strengths

Renewal completion workflows

Document collection infrastructure

Virtual mailbox functionality

Member-facing administrative support

Strong provider revenue-cycle alignment

Watch

Procurement maturity still developing

Long-term competitive durability remains unproven

WHO IS BUYING?

Medicaid Managed Care Organizations

Primary value:

Member-month preservation

Premium retention

Reduced procedural churn

Reinstatement recovery

Enrollment stability

Providers & Health Systems

Primary value:

Reduced uncompensated care

Coverage restoration

Revenue-cycle protection

Eligibility continuity

State Agencies

Primary value:

Administrative workload reduction

Renewal completion

Verification support

Call-center pressure reduction

Eligibility-processing efficiency

CATEGORY OUTLOOK

Coverage continuity is increasingly being evaluated as a distinct operational and procurement challenge rather than a subset of enrollment, care management, or member-services functions.

Several forces are contributing to that shift. Renewal frequency is increasing. Verification requirements are expanding. Work requirements introduce additional administrative workflows. At the same time, plans, providers, and state agencies are facing greater financial exposure when eligible individuals lose coverage because renewal, documentation, or eligibility processes are not completed successfully.

Unlike many social-care categories, the value proposition is tied to an event that occurs within the current contract cycle. Coverage is either maintained or it is not. Eligibility is either restored or it is not. Member months are either preserved or lost. As a result, performance can often be evaluated through operational and financial outcomes that are visible long before downstream utilization effects emerge.

The organizations highlighted in this category differ in their workflows, target populations, and operating models. What they share is a focus on reducing administrative coverage loss and preserving continuity of enrollment. As policy requirements and eligibility processes become more complex, these capabilities appear increasingly relevant to Medicaid managed care organizations, providers, and state agencies responsible for maintaining coverage continuity across large populations.

The category is still developing. Procurement pathways are becoming clearer, buyer demand is becoming easier to identify, and the underlying economic rationale is increasingly visible. The long-term competitive hierarchy remains unsettled, but the operational problem is unlikely to become less important.